{kind=link}

P

lanning for retirement is one of the most important financial decisions an individual can make. Whether you are in

your early career or approaching mid-life, creating a strong retirement corpus ensures financial independence and

peace of mind later in life.

In India, three popular retirement-focused investment options stand out: Employees’ Provident Fund (EPF), National

Pension System (NPS), and Public Provident Fund (PPF). Each of these schemes offers different benefits, tax

advantages, and investment structures.

But the question many investors ask is: Which one is the best retirement savings option?

The answer depends on factors like employment status, risk tolerance, tax planning needs, and retirement goals. Let’s

explore each option in detail to help you choose the right strategy.

Understanding EPF, NPS, and PPF

- Employees’ Provident Fund (EPF)

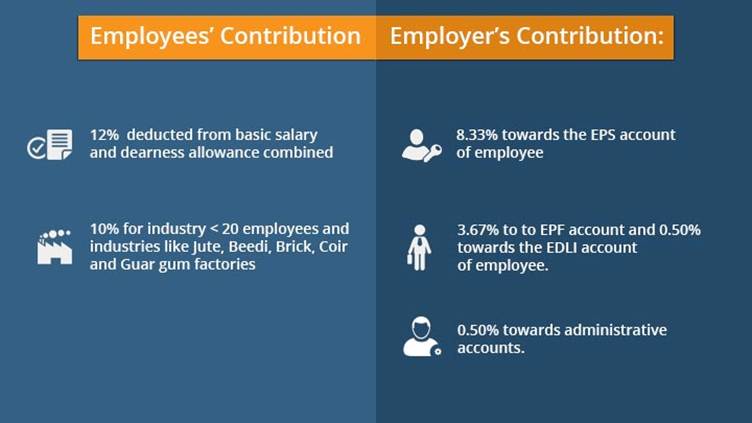

The Employees’ Provident Fund (EPF) is a retirement savings scheme designed mainly for salaried employees working in

the organised sector.

Under this scheme, both the employee and employer contribute 12% of the employee’s basic salary and dearness allowance

to the EPF account.

- Mandatory for most salaried employees in eligible organisations

- Government-backed savings scheme

- Current interest rate around 8%+ annually (subject to revision)

- Tax benefits under Section 80C

- Lump sum withdrawal allowed after retirement

- Stable and predictable returns

- Employer contribution increases retirement savings

- Tax-efficient investment

- Available mainly for salaried employees

- Limited flexibility in withdrawals before retirement

EPF works best for individuals working in the organised corporate sector, where employers contribute regularly to the retirement fund.

- National Pension System (NPS)

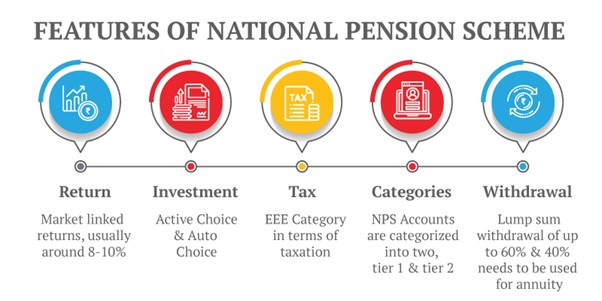

The National Pension System (NPS) is a government-sponsored retirement investment scheme that allows individuals to

invest in a diversified portfolio including equities, government bonds, and corporate debt.

Unlike EPF or PPF, NPS has market-linked returns, which means the returns can potentially be higher but also carry

some risk.

- Open to both salaried and self-employed individuals

- Flexible asset allocation between equity and debt

- Additional tax deduction up to ₹50,000 under Section 80CCD(1B)

- Partial withdrawal allowed after certain conditions

- Potentially higher returns due to equity exposure

- Extra tax benefits beyond Section 80C

- Suitable for long-term retirement planning

- Market risks affect returns

- Mandatory annuity purchase at retirement for part of the corpus

NPS is ideal for investors who want higher growth potential and are comfortable with market fluctuations.

- Public Provident Fund (PPF)

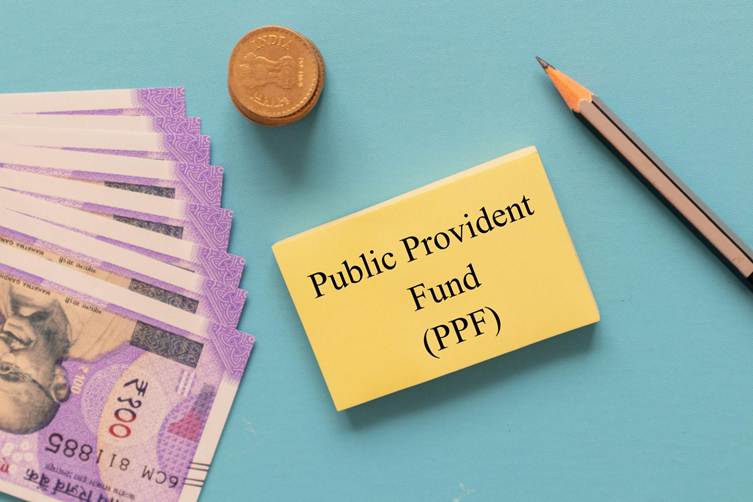

The Public Provident Fund (PPF) is one of the most trusted long-term savings schemes in India. It is backed by the

government and offers risk-free returns with tax benefits.

The scheme has a 15-year lock-in period, making it suitable for long-term financial goals such as retirement.

- Minimum investment ₹500 per year

- Maximum investment ₹1.5 lakh per year

- Current interest rate around 7–8% (revised quarterly)

- Completely tax-free returns (EEE category)

- Safe government-backed investment

- Tax-free interest and maturity amount

- Ideal for conservative investors

- Long lock-in period

- Limited annual investment amount

PPF works best for individuals who prefer low-risk investments and stable returns.

EPF vs NPS vs PPF: Quick Comparison

| Feature | EPF | NPS | PPF |

|---|---|---|---|

| Risk Level | Low | Moderate | Very Low |

| Returns | Fixed interest | Market-linked | Fixed interest |

| Lock-in | Until retirement | Until retirement (partial allowed) | 15 years |

| Tax Benefits | Section 80C | 80C + extra 50k | Section 80C |

| Suitable For | Salaried employees | Long-term growth investors | Conservative investors |

Which Option Should You Choose?

Choosing the right retirement savings option depends on your income type, risk tolerance, and investment goals.

Choose EPF if

- You are a salaried employee

- Your employer contributes to the fund

- You want stable, predictable returns

- You want higher long-term returns

- You are comfortable with market risks

- You want additional tax benefits

- You prefer safe investments

- You are self-employed or a freelancer

- You want tax-free long-term savings

Smart Strategy: Use All Three

Many financial planners recommend a diversified retirement strategy instead of relying on a single scheme.

For example:

- EPF for stable employer-backed retirement savings

- NPS for long-term growth through equity exposure

- PPF for safe, tax-free investments

Combining these schemes can create a balanced retirement portfolio with stability, growth, and tax efficiency.

Final Thoughts

Retirement planning should start as early as possible. The earlier you begin saving, the more your investments can

grow through the power of compounding.

Whether you choose EPF, NPS, PPF—or a combination of all three—the key is consistency and long-term discipline.

By understanding the strengths of each scheme and aligning them with your financial goals, you can build a strong

retirement corpus and secure your financial future.